In Malaysia's evolving e-Invoice ecosystem, one data element stands out as particularly critical: the Tax Identification Number (TIN).

This unique identifier has become the cornerstone of the entire e-Invoice framework, serving as the digital fingerprint that connects transactions to taxpayers in the national tax administration system.

What Is a Tax Identification Number (TIN)?

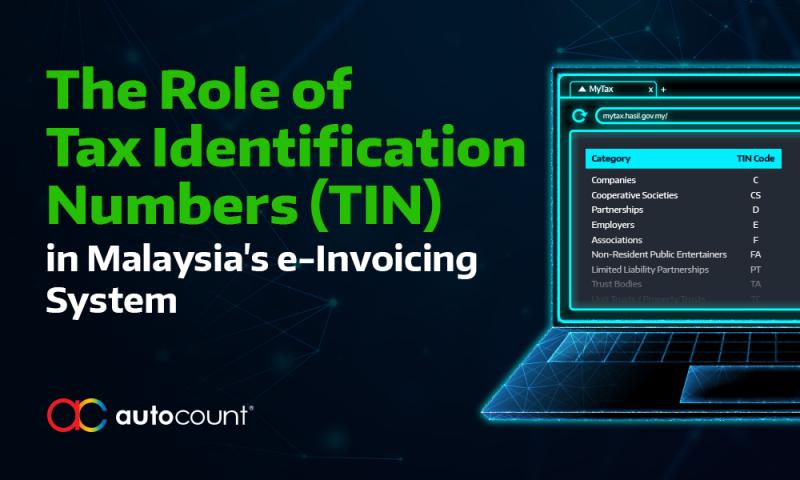

A Tax Identification Number is a unique identifier assigned by the Lembaga Hasil Dalam Negeri Malaysia (LHDN) to both businesses and individuals for tax administration purposes. In the context of e-Invoicing:

• Company TINs begin with the prefix "C"

• Individual or sole proprietorship TINs begin with the prefix "IG"

• Limited Liability Partnerships TINs begin with the prefix "PT"

• Partnerships TINs begin with the prefix "D"

• Associations' TINs begin with the prefix "F"

These identifiers allow LHDN to accurately track transactions, link them to specific taxpayers, and ensure proper tax compliance throughout the economy.

TINs as Mandatory Data Fields in e-Invoices

Every e-Invoice submitted to the MyInvois System must include TINs for both the supplier (issuer) and the buyer (recipient). This requirement applies regardless of transaction type, value, or business size. Without valid TINs, e-Invoices will fail validation and be rejected by the system.

The dual requirement for both supplier and buyer TINs creates a complete transaction record that enables LHDN to match income reported by one party with expenses claimed by another, enhancing tax compliance verification.

Special TIN Categories for Specific Scenarios

While standard TINs apply to most transactions, Malaysia's e-Invoice system includes several "general TINs" to accommodate special scenarios:

1. General Public TIN (EI00000000010)

Used in consolidated e-Invoices where buyers don't request individual e-Invoices

Also used when Malaysian individuals provide only MyKad/MyTentera numbers without TIN

2. Foreign Buyer TIN (EI00000000020)

Used for export transactions where foreign buyers don't have Malaysian TINs

Also applied for non-Malaysian individuals without TINs

3. Foreign Supplier TIN (EI00000000030)

Used in self-billed e-Invoices for import transactions where foreign suppliers don't have Malaysian TINs

4. Government/Statutory Body TIN (EI00000000040)

Used for transactions with government entities, state governments, local authorities, and statutory bodies

These general TINs ensure the e-Invoice system can accommodate all transaction types while maintaining data standardisation.

Practical Challenges in TIN Management

For businesses implementing e-Invoice systems, TIN-related challenges are among the most common issues encountered:

Challenge 1: Incomplete Customer TIN Records

Many businesses discover they lack TIN information for existing customers, creating a significant data gap when e-Invoice implementation begins.

Solution approach:

• Conduct a comprehensive audit of your customer database

• Prioritise obtaining TINs from regular transaction partners

• Develop systematic data collection procedures for new customers

• Consider using the MyTax Portal to verify TIN information

Challenge 2: TIN vs. Business Registration Number Confusion

Some businesses confuse TINs with business registration numbers (such as SSM registration numbers), leading to validation failures.

Solution approach:

• Clearly distinguish between TIN and registration number fields in your systems

• Train staff on the difference between these identifiers

• Request both numbers from customers to ensure completeness

• Remember that both must be included in e-Invoices as separate fields

Challenge 3: Foreign Entity TIN Management

Transactions with foreign entities require special handling of TIN information.

Solution approach:

• For foreign buyers, use the general TIN EI00000000020

• For foreign suppliers in self-billed scenarios, use general TIN EI00000000030

• Still collect and include any available business registration numbers

Challenge 4: Individual TIN Alternatives

Malaysian individuals may provide either a TIN or a MyKad/MyTentera numbers, requiring flexible handling.

Solution approach:

• Configure systems to accept either identifier

• Use general TIN EI00000000010 when only MyKad/MyTentera is provided

• Include the MyKad/MyTentera number in the registration/identification field

• For non-Malaysian individuals, collect passport/MyPR/MyKAS numbers TIN Validation Best Practices

To minimise e-Invoice rejections related to TIN issues, implement these validation practices:

1. Pre-submission verification

Verify TIN format (correct prefix and length) before submission

Confirm TIN matches the supplier/buyer name

2. Customer data management

Maintain TINs in a centralised database.

Update customer records with verified TIN information

Implement regular data quality checks

3. Staff training

Educate relevant personnel about TIN requirements.

Train customer-facing staff to collect TIN information

Develop standard procedures for handling TIN-related issues

4. System configuration

Set up validation rules in your systems to catch TIN format errors

Configure alerts for missing or potentially incorrect TINs

Consider integrating with LHDN's verification services if available

Finding and Verifying TINs

For businesses still building their TIN database, several approaches can help obtain this critical information:

1. Direct customer outreach

Contact existing customers to request their TINs

Incorporate TIN collection into the new customer onboarding

Include TIN requests in regular communications

2. Using the MyTax Portal

Businesses can check their own TIN through the MyTax Portal

The e-Daftar function allows registration and TIN verification

Follow the login process through https://mytax.hasil.gov.my/

3. Document review

Review existing tax documentation from transaction partners

Check previous formal correspondence that might include TIN information

Examine tax-related forms or registrations

Looking Ahead: The Evolving Role of TINs

As Malaysia's e-Invoice system matures, TINs will likely take on even greater significance:

• Enhanced compliance verification through automated cross-referencing of reported income and expenses

• Risk assessment algorithms that may flag unusual patterns in transactions between specific TINs

• Simplified tax filing as transaction data is pre-populated based on TIN-linked e-Invoices

Tax Identification Numbers represent the fundamental linking mechanism in Malaysia's e-Invoice ecosystem, connecting each transaction to specific taxpayers within the national tax administration system. By understanding TIN requirements and implementing robust TIN management practices, businesses can minimise e-Invoice validation failures while contributing to a more efficient and transparent tax ecosystem.

As e-Invoice implementation deadlines approach for businesses of all sizes in 2025 and 2026, prioritising TIN collection and validation now will pay dividends in smoother compliance later. Whether you're a small business using the MyInvois Portal or a large enterprise implementing API integration, TIN management deserves focused attention in your e-Invoice implementation strategy.

About the Author

Mr. Chin Chee Seng is the Independent Non-Executive Director of AutoCount and the Founder of CCS Group.

This e-Invoice News series is a collaboration with AutoCount.